How to Finance an NYC ADU: HELOC, Grants, Loans & More

Key Takeaways

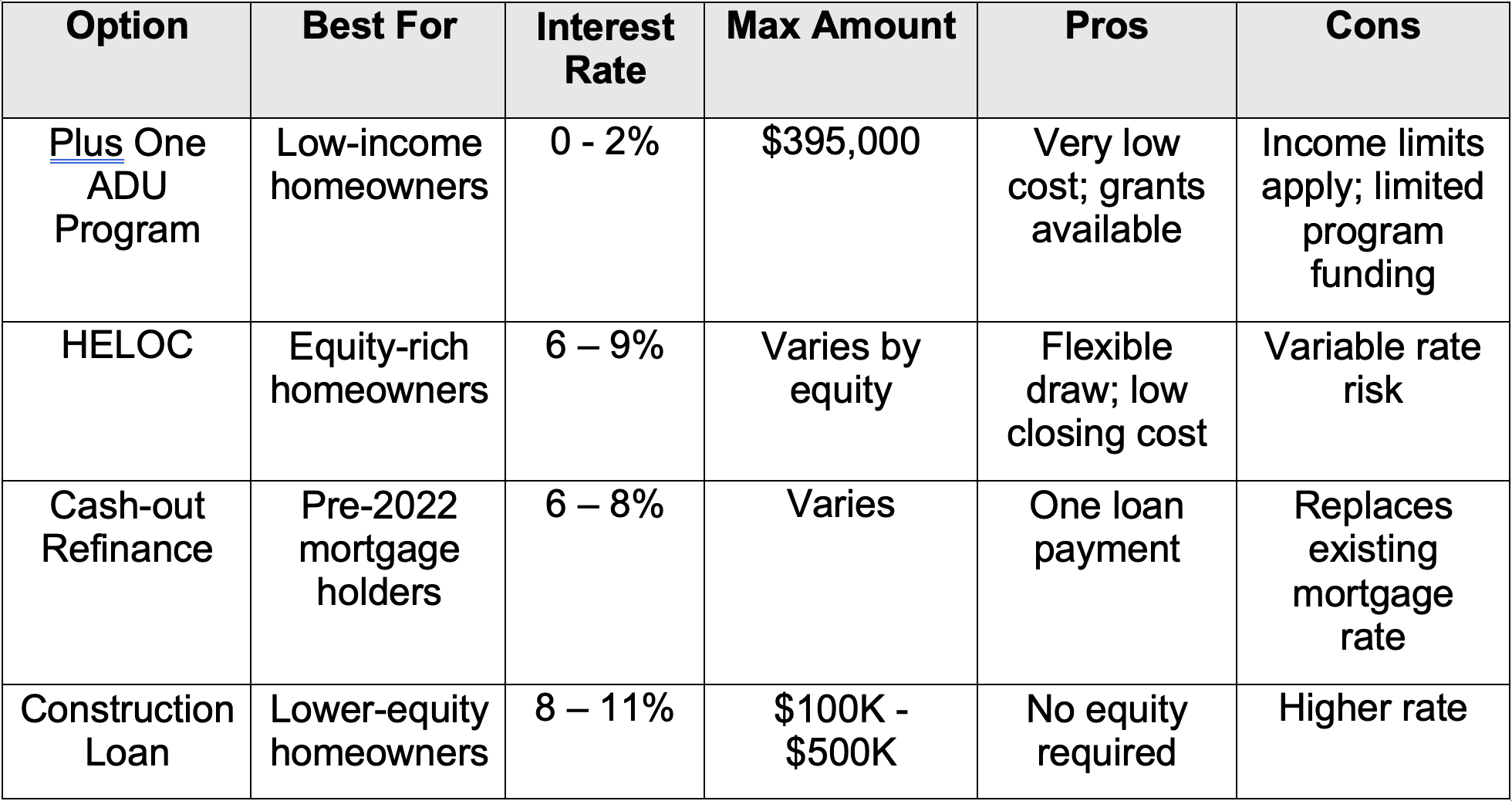

- Six financing routes exist; the Plus One ADU Program is the most powerful — up to $395K in low/zero-interest loans, forgivable loans, and grants for income-eligible 1–2 family owners.

- HELOCs and HELOANs (7–9% in 2026) let equity-rich owners borrow against their home — flexible draws or a fixed lump sum.

- Cash-out refinancing suits owners with a low pre-2022 mortgage rate and deep equity, but you trade away that rate.

- Construction-to-permanent loans fund the build for owners without equity; specialty ADU lenders offer more flexible underwriting.

- Before borrowing: set a real budget (25–40% of owners underestimate costs), confirm your equity, and ask how your lender classifies ADUs.

You've done the math. You've checked the zoning. You've even chosen the tile for the bathroom in your future ADU. There's only one issue — you need to figure out how to pay for it.

The good news: there are more financing options for NYC ADU projects in 2026 than ever before, including significant city grant funding that most homeowners don't know exists. Here's a complete breakdown of your options.

1. Plus One ADU Program — Up to $395,000 in City Assistance

This is the option most homeowners overlook — and it's the most powerful one available.

The Plus One ADU Program, administered by NYC HPD and NY State Homes and Community Renewal, provides eligible homeowners with:

Low- or zero-interest construction loans

Forgivable loans

Outright construction financing grants

Up to $395,000 in total assistance

Who qualifies? Eligibility is based on income limits (typically 80–120% of Area Median Income), property type (1–2 family), and property location within NYC. The program has been particularly active in Queens, Brooklyn, and the Bronx.

How to apply: Applications are submitted through Neighborhood Restore, the program's technical assistance partner. Second Key can help you assess your eligibility and prepare your application as part of our pre-construction advisory phase.

This program alone can make an ADU project financially viable for homeowners who wouldn't otherwise be able to afford construction costs. If you think you might qualify, check eligibility before exploring other financing options.

2. HELOC - Home Equity Line of Credit

For homeowners who've built up equity in their property, a HELOC is often the most flexible and cost-effective financing option.

A HELOC works like a credit card secured by your home's equity — you draw funds as needed during the construction process and pay interest only on what you've used. Interest rates are typically lower than personal loans or construction loans, and the interest may be tax-deductible.

Best for: Homeowners with significant equity who want flexible access to funds

Typical rates (2026): 7–9% variable

Draw period: 5–10 years

How to get one: Contact your existing mortgage lender first, then compare offers from local banks and credit unions

Second Key can introduce you to HELOC lenders who are familiar with ADU projects.

3. Home Equity Loan - HELoan

A Home Equity Loan, or HELoan, is similar to a HELOC in that you’re borrowing against the equity in your home without refinancing your mortgage. With a HELoan, you receive loan proceeds in one lump sum, with interest accruing as soon as you receive the funds.

HELoans have fixed interest rates for the life of the loan, and monthly payments include both principal and interest, similar to traditional mortgage loans.

Best for: Homeowners with significant equity who want flexible access to funds

Typical rates (2026): 7–9% variable

4. Cash-Out Refinance

When you've owned your NYC home for a while, a cash-out refinance can be a powerful tool. You replace your existing mortgage with a new, larger one and receive the difference as cash — which can be used for ADU construction.

Best for: Homeowners who bought before interest rates rose significantly (pre-2022) and have substantial equity

Key tradeoff: You're replacing your existing mortgage rate with a new one — if current rates are higher than your existing rate, this can significantly increase your monthly payment

Typical closing costs: 2–5% of the loan amount

In a high-rate environment, cash-out refinancing is often less attractive than a HELOC. But if rates come down, this may become the preferred option.

5. Construction Loan

A construction-to-permanent loan funds the build and then converts to a standard mortgage at completion. Unlike a HELOC, it's a standalone loan with a fixed schedule of draws tied to construction milestones.

Best for: Homeowners without existing equity, or those building a higher-cost ADU ($200K+)

Key consideration: Lenders will require detailed plans and a licensed contractor on board

Typical rates: 1–2% above standard mortgage rates during construction, then converts to market rate

6. ADU-Specific Lenders

A small but growing group of specialty lenders focus on ADU construction projects. They understand ADU timelines, the NYC permitting process, and expected rental returns, which can mean greater flexibility on underwriting than a traditional bank.

Which Lending Option Fits You?

Significant home equity, low existing debt: HELOC, HELoan, or cash-out refinance

Lower income or limited equity: Plus One ADU Program, ADU-specific lenders

Want to keep your current mortgage in place: construction loan or HELOC

Comparing Your Options

Before You Borrow - Three Must-Do’s

Before committing to a financing structure, plug your numbers into our NYC ADU ROI Calculator. Try the same project with different interest rates and down payments — you'll see exactly how much your financing choice affects monthly cash flow and payback timeline.

Establish a Budget - Consult a qualified contractor who specializes in ADUs for a feasibility study. Around 25–40% of NYC homeowners underestimate total costs.

Determine Your Equity - Zillow or broker estimates are a start, but if you’re refinancing, get an official appraisal.

Speak to Your Lender Early - Not all banks classify ADUs the same way. Some see them as “improvements”, others as “additions.” This affects loan terms and eligibility.

How Second Key Can Help

Financing is one of the most confusing parts of an ADU project and one of the most important to get right. We help clients:

Determine eligibility for the Plus One ADU Program

Introduce them to HELOC and construction lenders familiar with ADU projects

Structure the overall project budget so financing fits the build plan

We don't earn commissions from lenders. Our job is to get you the best outcome, not the best referral fee. Request a free assessment to discuss your project and financing options.